How I pay less tax on my savings in the UK [3 ways]

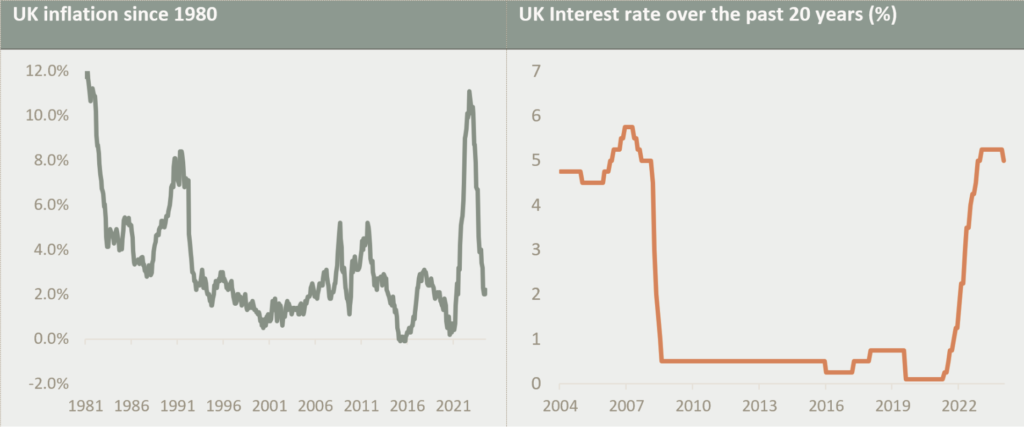

My monthly mortgage cost doubled when I remortgaged last autumn. Whilst it has made it harder for me to save as much as I would’ve liked: my wages increased by nearly 5% in the current financial year, and my savings account is paying me an effective rate of 4%. Contextually, inflation has also fallen from the hights of 11.1% in 2022 to around the target of 2%.

Problem

A combination of these events has meant that I am also due to pay even more taxes to the government because income tax threshold was not inflation adjusted, and the tax-free allowance were also not changed. Taxes are important for the government, but they also most negatively impact those who are less financially savvy and/or less financially well-off– simply because they can’t afford a tax adviser or are too obedient to keep on paying with no question asked! The UK government acts faster and with more force when an ordinary person makes a late tax-return than large corporations finding ways to pay less taxes than they should.

Alas – this post is not about the large corporates or the government, but 3 ways I have tried to pay less income taxes coming from my savings account.

My tax returns

I have just completed my tax returns, and I was happy that my earlier planning to reduce extra taxes for the past financial year has paid off by maximizing my tax allowances and investing smartly. I am lucky enough to have some cash savings, which easily goes above the £500 tax free allowance threshold for interest income (I am a high rate taxpayer). These savings have already been taxes and are simply from my net income, so it kind of pains me to have them taxed again – at the higher 40% income tax rate. So, I feel quite strongly about reducing those. I have found 3 ways of doing so (outside of an ISA). And I wanted to share these thoughts with you.

Solution 1: Fixed cash rate account

I staggered some of the cash across fixed rate cash accounts that pays total interest at maturity. And these products are paced out between 1-3 years. This means when rates do come down, as they are doing now, I will be able to make most out of my tax-free allowance at that point while also securing in a higher rate now. I have simply differed my interest income as I don’t need them now. This also helps with planning as I know upfront exactly how much interest I will receive at a certain point in the future.

Solution 2: Premium bonds

I have heavily piled some money away in premium bonds. For those who are not familiar, these bonds effectively feel like a lottery. Whilst they do not promise you a certainty of return like a fixed rate bond, any winnings you make is tax free. It works like this: every monthly there is a random pick on which bond numbers would be winning a certain cash amount. The winnings can range from £25 to £1 million. But it’s also true that in some months most people get no winnings at all.

However, unlike the lottery, they have an average rate of return which is currently set at 4.4%. This is pretty good compared to the 4% gross rate I am getting from my HSBC savings account. This simply means over the long-term you can expect to get this much return if you stay invested. I can say that for me, this has so far been true. In my next post, I can give more details about my personal returns.

In a nutshell, the amount I have won from premium bonds would’ve eaten into a significant portion of my tax-free allowance if I had left those money in savings account.

Solution 3: Gilts

Since I aim to maximize my ISA allowance every year, I needed to find another way to safely put my money away without paying taxes. As a result, I have opened a General Investment Account (GIA) and have directly bought a UK government bond, known as gilt, maturing in January 2025. The particular one I have invested in pays a very small coupon but better capital gains potential.

For your information, any capital gains you make from buying bonds are tax-exempt. This means when I bought the bond at a “discount” I knew exactly how much capital gains I would be making from this bond – this is because all bond prices trade to their “face value” at maturity.

As a result, I put away some cash in a relatively safe asset (government bond) – knowing how much tax-free capital gains it will have.

The summary

All these tips are especially valuable when you already max out ISA allowance and savings allowance. These are:

- Staggered fixed rate cash accounts

- Premium bonds

- Direct gilt purchase

If you find this post helpful do share with your friends and family so they can also benefit.

I hope you subscribe to my blog, and I am most easily reachable on Instagram so hope to see you there?

With hope, Subtle Investor