How to invest during inflation and manage finances better?

There is a reason why inflation is known as the “Silent Killer”. It creeps up and takes away your purchasing power over time. Inflation has been under the limelight so far this year and why wouldn’t it be? Consumer Price Inflation (CPI) have risen to 5.4% year-on-year last month in the US, compared to the Central Bank’s average 2% target. In the UK, the number stands at 2.4%. Don’t underestimate the intensity of this little number which affects everything – from individuals to countries and rest of the world!

This post is all about our current level of high inflation and whether it will remain high for a long time. If so, how should we invest during inflation and what it will mean for our finances?

What is inflation?

Inflation is simply a percentage change in prices of goods & services in a country. It measures cost of a basket of goods that consumers (i.e. us) have to pay every month. It is typically measured using Consumer Price Index or CPI. A percentage change in this index value month-on-month or year-on-year is a monthly or an annual inflation number. Generally it is quoted as an annual number. For advanced countries like the US and UK that number is targeted by the central banks to be roughly 2% every year. For financial stability of a country, independent central banks don’t want consumers to see prices rising too fast.

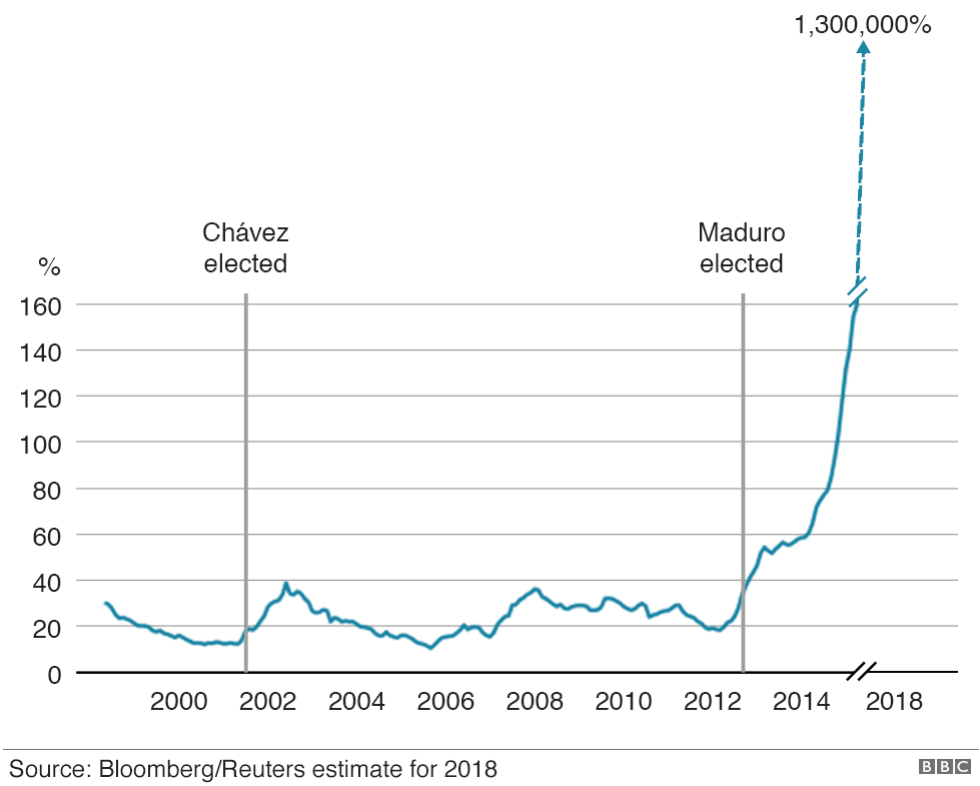

However, when things go out of control, and a country enters hyperinflation or an extremely rapid increases in prices, you can see some crazy situations that are faced by countries such as Venezuela. This South American country saw annual inflation reaching 1,300,000% in November 2018. It led to situations where Venezuelans had to pay 2.6m Bolivars for a toilet roll paper or 14.6m for some chicken. Here’s a snippet from a BBC article.

How high can inflation go in the UK and US?

Not 1,000%. When we talk about high inflation in our country, we are talking about inflation increasing above 2%. Or maybe sticking around 3% for a while. This is because even a high persistent inflation of 3% will have some impact on us. That’s because it is the ultimate job of the independent central banks to keep that number around 2%. So the idea is, if we consistently see annual inflation above 2% month after month – it will trigger the central banks to become hawkish and start rising interest rates. We call this tightening of the monetary policy.

Notice the word “consistently”.

This is a very important part of the messaging that central banks like the Fed and Bank of England are trying to convey to rest of us. It will only become a headache for these banks if inflation remains higher for longer. So far, none of these banks think that high inflation is here to stay. They are calling higher inflation “transitory”. The word transitory have become a buzzword in the news and our finance community. And whether inflation is transitory or not will impact what we should be doing or where you should be investing your money.

Why inflation is only expected to be transitory?

Technical reasons such as base effect

Since inflation measure is a percentage term, so it depends on what “base” value it comes from. The nature of the COVID crisis meant we literally could not spend money as shops were closed. This means inflation data that was reported one year ago was already pretty low. And so when you do a percentage increase from a low value, the number automatically looks high. So this is the base effect that you’d hear a lot of people quote. Therefore, the understanding is that once we start to settle down and reach our normal level of spending, we are unlikely to see inflation remain high.

Supply disruptions

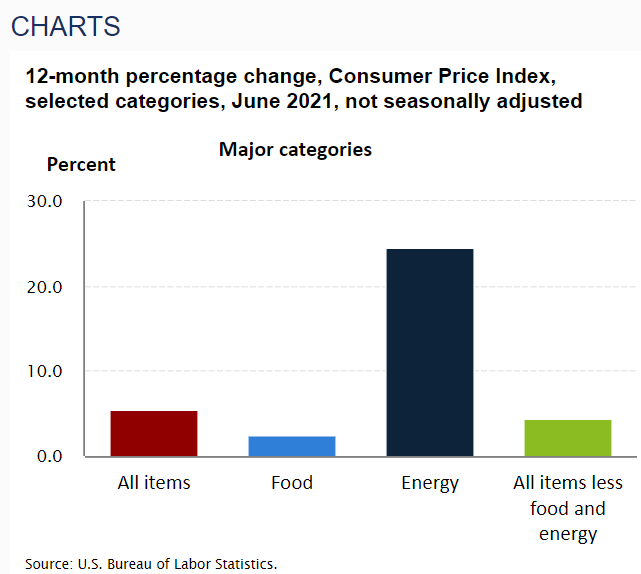

Again covid related. What is currently going on in the world right now is a huge supply-demand mismatch. The pandemic impacted every part of the supply chain you can think of. It impacted sourcing of raw materials such as oil and metals, to selling good to consumers like us. This meant that prices of some of these raw materials or commodities that are used in production of goods were pushing higher. This increasing the overall cost for both us the consumers and producers who produces the final goods. And for us, think about what makes up overall consumer inflation number. You’ll see that at the moment, a high increase is in fact coming from these commodities. The chart below shows what makes up inflation in the US. Same can be found for UK here.

Excess stimulus

Third reason why high inflation could be short lived is simply because a lot of higher demand are coming from excess stimulus in the economy. Governments all around the world especially the US handed out generous help in forms of cheques or job protection for their people. This in aggregate meant, we have saved up money that we may have spent if the shops were open last year. The extra savings won’t last for long as we return to some sort of normality. The same goes for inflation.

But, How to invest if inflation does stay high?

Investments to avoid

Firstly I would stay out of cash. By principle, purchasing power of paper money will definitely be decreasing by the inflation rate.

Next I would want to avoid fixed income products like bonds (unless they are inflation linked) – high inflation hits the bond market first. When you purchase a bond you are fixed with how much interest you’ll get during the time you hold that bond. Therefore it will not be able to keep up with rising inflation. If a nominal bond pays 1% interest, but inflation is 3%, you are guaranteeing yourself a 2% negative real return.

It will also hit stocks. Different stocks will be impacted at different level. Not all stocks are equally sensitive to inflation. However, over the short term stocks will have some knock on impact as companies will struggle to pass on rising costs. However, history highlight that over a very long-term stocks generally perform well and provides a good positive real returns. I have a video on inflation and stock market – feel free to check that out below.

Add "real assets"

Unlike typical assets such as stocks and bonds, there are certain other asset classes that will survive higher inflation better. We call these “real assets”. This includes investments with direct link to a tangible asset. Examples include property, infrastructure, and some commodities. You can expect to have better investment returns from properties because like prices of goods you can also increase the rent in line with inflation. Assets like these are tied to a “real asset”, which sees its value going up and it is precisely why they help to hedge against inflation. Commodities can also directly help over the short term. The reason is quite intuitive. If you think of the inflation basket such as CPI (chart above) one of a key components of it is energy. Energy is a commodity. So when energy prices go up, inflation goes up and if you invest in energy, your investment value also goes up.

Biggest tip? Diversify your investments

Remember different sectors or countries will have different levels of inflation and different sensitivity to inflation. If you only invest in the US stock market and US persistently runs high inflation it will impact your investment. However, if you also invest in European stocks (where high inflation fear is not as hot as US) your investments wouldn’t take a similar hit.

...what else can you do?

Find a better place to store money

A simple bank deposit account provides the worst return on your money. My main bank account is with Barclays and they provide only 0.01% on their everyday savers account. If inflation stays high at 3%, you are guaranteeing yourself a negative 2.99% return. Even without a high inflation, it may work out better to actually invest during inflation. Cash accounts generally gives negative real returns because interest rates are at all time low. Therefore, while it could be too much of a hassle to change bank accounts every so often, it makes sense to only keep the bare minimum needed in these cash accounts. And put the rest in a high yielding investment account such as through an ISA.

Fix your future cost

Beginning of the year I was due to renew contract with my energy provider. Of course I shopped around and found a slightly cheaper deal. But, not only that I chose to go with a fixed term contract. I fixed the future cost of my gas and electricity. At that time I was aware that energy prices are increasing and likely to stay higher. As you just read, energy prices are a key component of inflation or CPI index and they are contributing to higher inflation in almost every country around the world.

Good time for a “good debt”?

Keeping with the idea of fixing things, if you are thinking of getting a mortgage or buying your home, it may be a good time to do that. This is because the money you borrow against a home mortgage would start to worth less and less if inflation is high. It’s a win-win situation because the interest cost you pay in your mortgage will be fixed & nominal but your income will be not (hopefully). Basically with high inflation, you can expect to have higher wage growth to help you keep up with rising cost. However, it wouldn’t necessarily increase the cost you pay towards mortgage interest. But, if you rent, your landlord can easily increase the rent (your landlord invested in a ‘real asset). With mortgages the banks don’t have the luxury to do that as you have fixed the amount already in a binding contract.

I must add and really emphasise the importance of keeping all your debts under control. If you are already overwhelmed with debt then, before getting into more it’s worth finding out ways to first reduce your current level of debt.

Watch out on your reoccurring bills

One thing that is certain with inflation is: rising prices. This comes all the way from the start of a supply chain such as a factory to all the way in our bills. Some companies will try to pass on most of these high cost directly to you. The companies will think that you like their goods and service so much that you’d happily pay for the increased price. So keep an eye on those bills and letter and shop around to find better rates!

The summary

- Current readings of high inflation is expected to be transitory

- Cash and fixed income investments such as bonds provide investors with worst outcome in terms of investment returns (during high inflation)

- Real assets can help to hedge inflation risk such as properties and commodities

- High inflation with low interest rates means it could be a good time to get into a “good debt” such as home mortgage

- As always, with or without high inflation it is a good practice to invest any excess money (that is not need in near future) rather than keep them in bank accounts