Will Interest Rate go down? | How will it affect the economy?

What is an interest rate?

For borrows, it is a “cost” and for savers it is an “income”. We pay and receive interest everyday through credit card loans, mortgages and personal savings account. Therefore, if interest rate go down or up , it will directly impact us all.

Before getting into the detail, it is important to note that interest rate is set by each country’s Central Bank (such as FED or BoE), we call that the “base rate”. Banks follow the central bank’s base rate in order to set charges on our borrowing such as mortgages.

Interest rate history

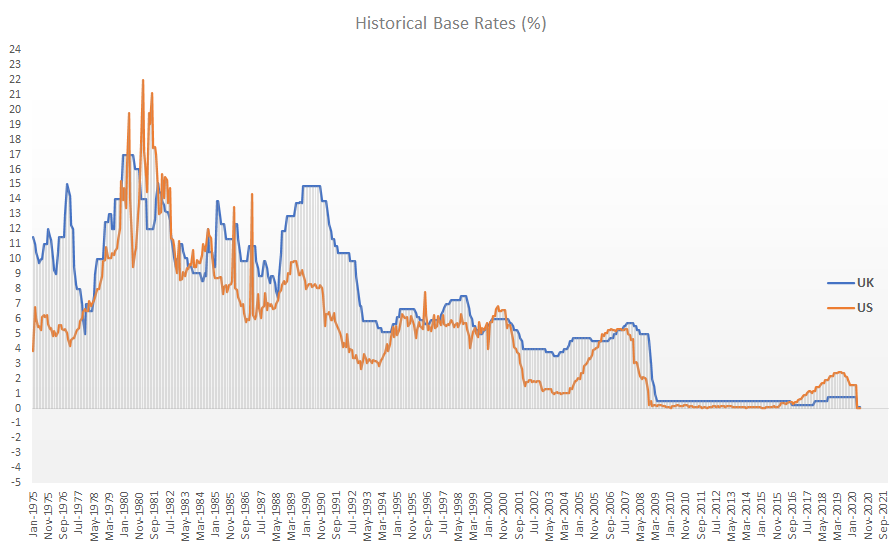

As of summer 2020, we are seeing record low interest rates followed by central bank cuts. Given everything that is happening in the economy right now, Central Banks are using their monetary policy tool to help revive the economy. Before the Global Financial Crisis (GFC) of 2008, rates have never been this low. Observe the chart below from the 70s. Can you imagine that our grandparents lived in economies with base rate as high as 15%? What would it have meant for mortgages? Will you still be able to afford your current mortgages or loans with rate this high?

Will interest rate go down?

The market was expecting a rate cut since the pandemic started to make its impact. Both the US and the UK is facing severe recession risks. With no economic activity such as eating out at a restaurant or watching movies at a cinema, our countries are not really producing a lot of “economic goods” right now. As a direct result of this, we are seeing knock on affect through job losses and rising mortgage holidays. Study of economics teaches us to measure health of an economy by observing growth in its Gross Domestic Product (GDP). A healthy target for GDP growth in advanced economy like the US and UK is 2-4% per year. Contrary to that, in May 2020, the Bank of England estimated that UK’s GDP could fall by 25% over just the second quarter alone. This is huge and record breaking.

So, the short answer to the question is that there is a possibility for further cuts. In fact, the Deputy Governor of BoE did not rule out negative interest rates. But worry not, we will not be the first country to have negative interest rates. European Central Bank, for example, cut its rate below 0 in June 2014 in order to deal with the Euro Zone crisis.

How interest rate affect the economy?

Since the Central Banks utilises Interest Rates as a tool for controlling our economy, a subtle change in rates generally has a noticeable impact in our economy. The stock market is noted to directly react when rates changes. When interest rate is cut, it is a positive signal for the equity markets and so it goes up. This is precisely what has been happening following the sharp sell-off we saw in the stock market due to COVID. We are in a crisis right now. There is a tremendous pressure on our country’s central bank to carry on reviving the economy. They are doing everything from: lowering rates to pumping money into the economy.

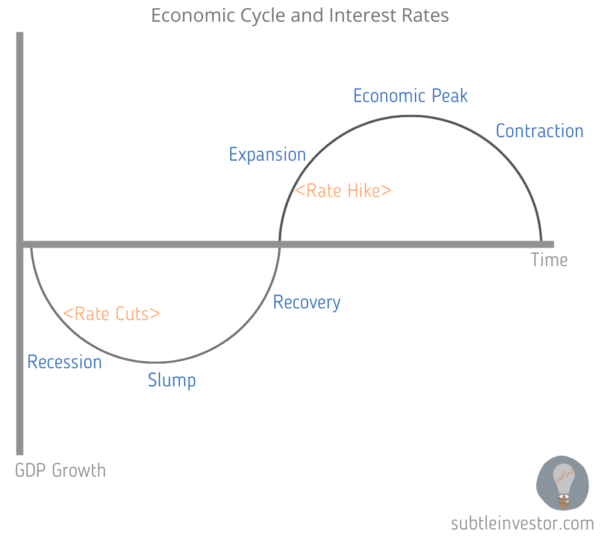

To help visualise our economic cycle with interest rate, observe the illustration below. As we are approaching a recession and a slump, it is natural to expect rate cuts.

A healthy economy is key for a president to win election in the US. Since the election day is looming; you may have noticed Mr Trump tweeting in favour of rate cuts…even welcoming negative interest rate!

As long as other countries are receiving the benefits of Negative Rates, the USA should also accept the “GIFT”. Big numbers!

— Donald J. Trump (@realDonaldTrump) May 12, 2020

Why interest rate is important?

Precisely because it affects the economy and our lives. It impacts our decision to save, borrow or spend. For example, if interest rate rises too much, there will be families that may struggle with mortgage payments. In fact. it is not just the households, businesses will also see increase in cost of borrowing. Increasing cost leads to postponing of new projects, halt of business expansions and further cuts through employee redundancies.

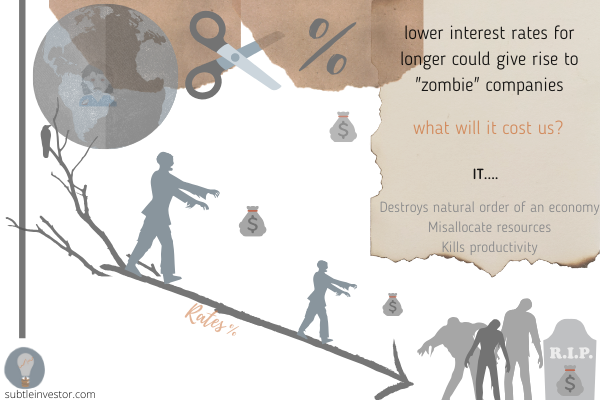

In line with the note above, it may seem that low rates are a positive thing. Low rates mean low cost and a happy household. However, as a Subtle Investor, do not limit your thought to just the surface of the problem. Preference of the current president/government might be to keep the rates very low. However, it is important to remember that governments will come and go, but our life will have to continue in an orderly fashion. Therefore, it is prudent to also think of the long term. What will such lower rates do to us? Using up all the available tools at the central bank’s disposal at present means there is little space left for manoeuvre during a future crisis. Philosophically, what will it do to our future economy and productivity? There is a possibility that it will artificially make us feel much more prosperous than we really are – leading to rise of zombie companies and households. [You can read an old article from guardian on how zombie firms affect our economy here]

Will that be desirable?

The summary | What can we do as a Subtle Investor?

- In the short term, try to keep at least 3-6 month’s salary in an easy to access bank account. This is because the economy is not great at the moment and we should always keep an emergency fund for the rainy days. With US election in few months time and BREXIT saga continuing in the UK – it will be a patchy ride.

- With rest of the savings, it will be beneficial to slowly have them invested in the stock market or any other investment of your choice. This is because with low rates, we will be losing real value of our money if left in a bank account. This should be a good medium-to-long term strategy as the economy starts to pick up. You may find reading my other post on why now this a good time to start investing, a useful starting point

- If we can afford, it may also be a good time to buy a house that’s been on the wish list for some time now– we can use the low interest rate to lock into a low mortgage payment. In fact, it could even be cheaper than paying rents to the landlord!